Paul Greene

The biogas industry is keenly focused on economic opportunities resulting from the generation of upgraded biogas to renewable fuel and its attached environmental credits, called RINs, or Renewable Identification Numbers. Congress created the renewable fuel standard (RFS) program, which the U.S. Environmental Protection Agency implements under consultation with the U.S. Department of Energy, to reduce greenhouse gas (GHG) emissions and expand the nation’s renewable fuels sector while reducing reliance on imported oil.

The biogas industry is keenly focused on economic opportunities resulting from the generation of upgraded biogas to renewable fuel and its attached environmental credits, called RINs, or Renewable Identification Numbers. Congress created the renewable fuel standard (RFS) program, which the U.S. Environmental Protection Agency implements under consultation with the U.S. Department of Energy, to reduce greenhouse gas (GHG) emissions and expand the nation’s renewable fuels sector while reducing reliance on imported oil.

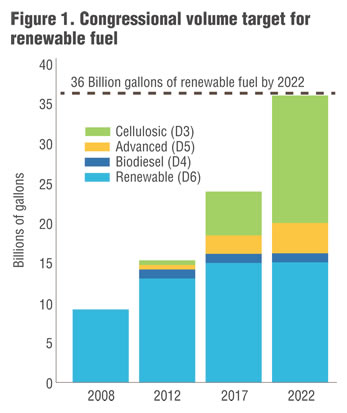

This program was authorized under the Energy Policy Act of 2005 and expanded, often called the RFS2, under the Energy Independence and Security Act of 2007. Key expansion items included higher long-term goals to more than double current volumes, calendar extension to 2022, grandfathering of certain original fuels, explicit defining of qualifying fuels, and introduction of specific waiver authorities. Renewable fuels fall into four categories, each with their own annual volume standards shown in Figure 1:

- Cellulosic Biofuel (D3): Produced from cellulose, hemicellulose, or lignin and must meet a 60 percent lifecycle GHG reduction.

- Advanced Biofuel (D5): Produced from a non-corn starch, renewable biomass and must meet a 50 percent lifecycle GHG reduction.

- Biodiesel (D4): Must be biomass-based diesel and meet a 50 percent lifecycle GHG reduction.

- Corn-Based Ethanol (D6): Ethanol derived from corn starch and must meet a 20 percent lifecycle GHG reduction.

The Program

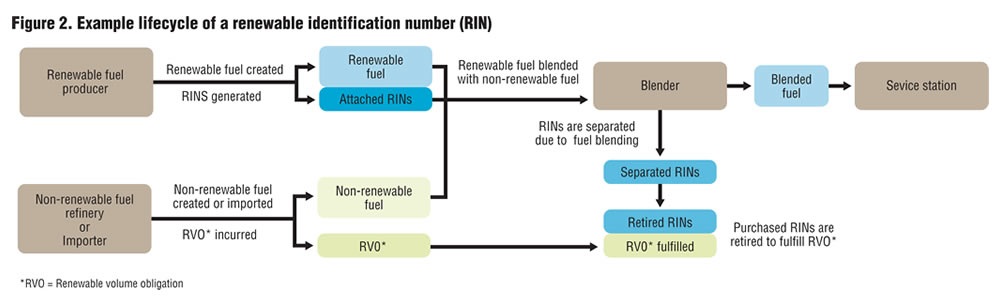

To both enforce the mandate for their use and develop the markets for these fuels, EPA developed a trading and enforcement program comprised of obligated parties and renewable producers. Obligated parties are refiners or importers of gasoline or diesel fuel, and are given the name “obligated” as they are required to comply by blending renewable fuels into transportation fuel, or by obtaining credits called RINs to meet an EPA-specified volume obligation — the Renewable Volume Obligations or RVOs. Obligated parties are to demonstrate compliance with the program by the end of the compliance year, but are given flexibility in carrying a compliance deficit into the next year. That deficit must be made up by the end of the extended year. Figure 2 illustrates how RIN credits are transacted.

RIN Credits

RINs are the backbone of the program. They are the currency used in trading. Every equivalent gallon of renewable fuels is assigned a RIN at its point of generation or origination. These RINs work much like Renewable Energy Credits (RECs) work in the generation and trading of renewable electricity. RINs can be traded between parties, bought as attached RINs to fuel purchased, and/or bought unattached on the open market. Unlike California’s Low Carbon Fuel Standards (LCFS) program, RINs expire. Unused RINs can carry over via the additional extended compliance year allowance, but beyond that, if not used, they expire. This expiration element is why RINs are traded with not only its RIN classification (next section), but also with its generation and therefore expiration date.

There are ten steps along the journey to generating and selling RINs. Each is key to a successful RIN creation and sale:

- Proper Feedstocks, e.g., biosolids, food waste or manure

- Proper Conversion Technology, e.g., anaerobic digester or landfill with gas capture

- Gas Upgrading Technology to meet RNG specification

- Gas Compression

- Installation of Injection Point — and subsequent injection into gas pipeline of a gas utility that has issued permission

- Gas Offtaker, e.g., a transportation company or gas fuel company

- RIN Validation Partner — an expert at all the needed Quality Assurance/ Quality Control and reporting requirements

- RIN buyer, e.g., an obligated party that will retire the RIN

- Gas Filling Station

- Natural Gas Fueled Vehicle

RIN Types And Volumes

RINs

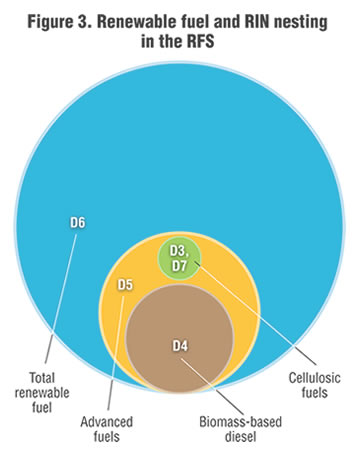

A RIN exists for each of the four renewable fuel categories described, and named with the letter D as a prefix and numbered 3, 4, 5, 6, and 7. D3 RINs are called cellulosic RINs and D5 RINs are called advanced biofuels RINs. Both are of paramount interest to the biogas industry, as biogas producers have approved pathways (see Pathway section) for production of these two categories. D3 RINs are trading at about three times the value of D5 RINs — about $2.85 each for D3 and $0.85 each for D5 at the time of this writing (Fall 2017). A key difference between D3 and D5 RINs is the D3s come from cellulosic sources and D5 can be from other types of carbonaceous feed material, not necessarily from cellulose. All landfill gas RINs qualify for D3 status, thanks to some effective lobbying on the part of the solid waste industry. Not all biogas digesters get such status for their biogas RINs.

A RIN exists for each of the four renewable fuel categories described, and named with the letter D as a prefix and numbered 3, 4, 5, 6, and 7. D3 RINs are called cellulosic RINs and D5 RINs are called advanced biofuels RINs. Both are of paramount interest to the biogas industry, as biogas producers have approved pathways (see Pathway section) for production of these two categories. D3 RINs are trading at about three times the value of D5 RINs — about $2.85 each for D3 and $0.85 each for D5 at the time of this writing (Fall 2017). A key difference between D3 and D5 RINs is the D3s come from cellulosic sources and D5 can be from other types of carbonaceous feed material, not necessarily from cellulose. All landfill gas RINs qualify for D3 status, thanks to some effective lobbying on the part of the solid waste industry. Not all biogas digesters get such status for their biogas RINs.

Figure 3 illustrates how RIN categories are “nested” within each other. Importantly, obligated parties must obtain sufficient RINs for each category that applies to them to demonstrate compliance with the annual standard. For example, a cellulosic RIN could be used to meet obligations for a total renewable fuels standard. Therefore an obligated party that would like to fulfill its D5 Advanced category can either buy D5, D4 or D3 RINs to meet that obligation.

RVOs

Renewable Volume Obligations (RVOs) are calculated by EPA via a rulemaking. The RVOs establish an annual quantity target of biofuels that EPA requires the fuel supply industry to purchase and blend. The annual quantities established are based on the coming year volume requirements and projections of gasoline and diesel production. In 2017, the RVOs are:

- 6 Renewable Category: 18.8 billion gallons

- D5 Advanced: 4 billion gallons

- D4 Biodiesel: 2 billion gallons

- D3 Cellulosic: 0.311 billion gallons

Cellulosic Waiver Credit

Recognizing short-term difficulty in attaining required volumes of cellulosic standards, EPA has added even more flexibility to the program beyond that generated by the nesting principle. This is the cellulosic waiver credit (CWC), which is offered by EPA, at a price determined by formula in the statute, so that obligated parties have the option of purchasing CWCs plus an advanced RIN in lieu of blending cellulosic or obtaining a cellulosic RIN. The published price of a CWC in 2017 by EPA was $2.00. The trading theory is that the value of a D3 RIN should be fairly close to the value of a D5 RIN plus the CWC.

Pathways

EPA’s intentions in developing RFS2 were to allow wastes to be converted to a wide array of fuels to maximize the nation’s opportunity to increase its homegrown, low carbon fuel supply. These fuels can be in gas, liquid or electric forms. Each type of waste, such as manures, food wastes and biosolids, could be converted to a renewable fuel by a variety of conversion technologies that include processes like gasification and anaerobic digestion.

Each occasion where a different feed material uses a different conversion process and makes a different kind of fuel, a “Pathway” is registered with the EPA. This is the Agency’s way to verify that the required reduction in carbon intensity is achieved. The pathway must only be created once so future deployment of the same feed-to-fuel pathway does not need to go through the review process again. Currently, over 20 different pathways are registered with EPA, with biogas-specific pathways among them.

Pathway Q

Of keen interest to the biogas market is Pathway Q. This is the pathway by which renewable compressed natural gas (CNG), renewable liquefied natural gas or renewable electricity are generated from biogas from landfills, municipal wastewater treatment facility digesters, agricultural digesters, and separated MSW digesters. Within this pathway are specific rulemaking and rulemaking interpretations on which feedstocks constitute production of cellulosic (D3) or advanced biofuel (D5) RINs.

Liquid Vs. Gaseous Fuels

Many vehicles are powered by natural gas due to its cost competitiveness. For example, CNG vehicles, such as trucks and buses, can operate for less fuel cost than liquid fuel such as diesel. The RFS is accommodating this market shift. Digester or landfill biogas that is upgraded, compressed and injected into a gas pipeline is a part of Pathway Q, producing renewable natural gas fuels, commonly called RNG. Careful examination of EPA statistics on existing and planned RFS fuel projects points to biogas projects and specifically their RNG as a critical path for generation of renewable fuels, particularly cellulosic and advanced biofuels. An interesting relationship within this RNG sector is the role fossil CNG plays in allowing for development of a CNG infrastructure that in turn intensifies interest in equivalent but renewable RNG.

Electric Vehicle (EV) Pathway

An untapped opportunity for the biogas industry is the electric pathway. EPA has approved the pathway of using biogas to fuel electric generation where the power is specifically used to fuel electric, plug-in vehicles. This is a topic of much contention because no RVO has been established by EPA for the EV pathway, so the market has yet to respond to making the fuel. The biogas industry has the potential to cost effectively fuel millions of EV cars. Similar to the just discussed importance of fossil CNG building out the required infrastructure, is the dynamic of the infrastructure being installed to charge EV vehicles. This will help drive biogas-electricity fuel demand and in turn boost demand for electric vehicles.

Equivalency

EPA has determined that each type of RIN must be compared to another through a comparison of its fuel value per unit volume to that of pure liquid ethanol fuel. Each gallon of ethanol has about 77,000 Btu (or 0.077 MMBTU), which is thus the definition of a RIN. A useful conversion to study the business case for RINs is to convert the value of the credits to dollars per MMBtu.

Here’s the math: $ X/RIN x RIN/0.077 MMBTU = $ X/MMBTU

For example, if a project were selling its D3 RINs at $2.90 each, that would be the equivalent of almost $38/MMBTU. With natural gas trading at about $3/MMBTU as of this writing, the value of the RINs are worth over 12 times the value of the natural gas.

Industry Policy Drivers

Several concerns exist for both digester and landfill biogas projects within the RFS program:

The primary concern is policy uncertainty in the RFS market, lately resulting from resistance from entrenched conventional petroleum fuel interests. As of this writing, however, the Trump Administration is on record in the press to make the 2018 RVOs at least as high as this year’s. This signals a positive switch from July 2017 preliminary rulings. This is good news for the industry.

Legislative action is presently only out to 2022, which does not provide much long-term certainty for debt financing of AD projects.

Recent uncertainty in annual RVO quantities that the industry will be required to meet.

High valuation of cellulosic D3 RINs incentivizes the industry to work closely with EPA on modifying or reinterpreting cellulosic rulemaking so that interpretations of feedstock and awarding of D3 RINs are more consistent, in line with EPA desires to remove organics from landfills, and simple with respect to required testing and reporting. Policy should favor landfill diversion of organics but is actually achieving the opposite, as landfills are guaranteed D3 RINs for all their biogas and anaerobic digesters that take in food waste have to provide onerous testing and validation on their feed material and only get a fraction of their RINs as D3.

The biogas business continues to show itself as a key leading contributor to U.S. energy security and a strong source of advanced, renewable biofuel with extremely low greenhouse gas emissions. Compared to conventional fossil natural gas, upgraded biogas or Renewable Natural Gas has extremely low emissions thus a very friendly environmental footprint.

Paul Greene (greenep@cdmsmith.com) is a Senior Technical Advisor for CDM Smith, a top 5 environmental engineering and construction company. He is a Director of the American Biogas Council and a former Chairman.