An understanding of what equipment costs to operate — by calculating machine rates — is part of sound financial management of an organics processing facility.

Craig Coker

BioCycle May 2015

Photo by Doug Pinkerton

Organics recycling, whether by anaerobic digestion, composting or a combination of both, should be accomplished by developing, and adhering to, a budget that accurately accounts for the costs of processing. This allows the management of the production facility to set pricing for revenue-generating activities (e.g., incoming feedstock tip fees, compost and/or biogas product sales) that covers those processing costs and overhead expenses, and generates a profit (or offsets expenses, e.g., with publicly-owned operations). Budgets are needed for initial business and facility planning and design efforts, for periodic financial performance reporting to stakeholders and investors, for allocations of government funds for operation and for effective human resources management.

Budgets are forecasts of anticipated costs over a period of time, usually a fiscal year. Some elements of a budget, like land lease or mortgage payments, are relatively easy to forecast. Others, like equipment maintenance, are more difficult due to likely variations from forecasts during the budget year. An important mechanism to help plan and develop accurate budget forecasts is to develop machine rates for each piece of equipment used to process incoming feedstocks. Machine rates are also used to compare two pieces of equipment for purchasing or leasing decisions.

Machine Rate Fundamentals

The machine rate is the cost of owning or leasing and operating a particular piece of equipment. The objective in developing a machine rate should be to arrive at a figure that, as nearly as possible, represents the cost of the work done under the operating conditions encountered. The machine rate is a compilation of fixed costs, operating costs and labor costs. These costs are expressed over a particular unit factor, usually dollars per hour, but sometimes dollars per unit volume or mass of material handled. The machine rate multiplied by the actual or estimated hours of use in a budget year gives the annual projected cost for that piece of equipment. These rates will be based on best professional judgment and/or established rates elsewhere for start-up facilities; for operating facilities, a more rigorous approach to information management and bookkeeping will be needed to track the details of these costs for each piece of operating equipment.

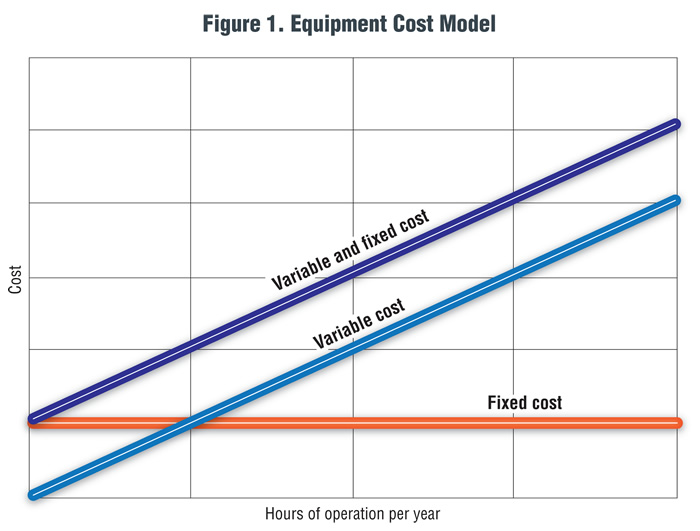

Fixed costs are those that accumulate over time and do not vary with the amount of material handled or hours the machine is used. Elements of fixed costs include: interest on monies used to purchase equipment or leasing rates, taxes, insurance, equipment depreciation (although this can be viewed as varying depending on usage) and storage costs (if any). Operating costs vary directly with the work done by the machine and these costs normally include: fuel, lubricants, maintenance, tires and repairs. Labor costs are those operating costs associated with employing labor, including direct wages, direct benefits (personal time off, vehicle compensation, etc.), employer taxes and social costs, including payments for health and retirement. The cost of supervision may also be spread over the labor costs. Figure 1 illustrates the relationship between these cost factors.

Figure 1. Equipment cost model

An important consideration is to separate the costs in such a way as to make the most sense in explaining the cost of operating the equipment. For example, equipment depreciation is driven by the equipment salvage value and equipment life. For a computer, salvage value is influenced by the rate of obsolescence so the depreciation cost is largely dependent on the passage of time, not the hours worked. For a front-end loader, a major determinant may be the actual hours of equipment use, as high-hour loaders have less salvage value than low-hour loaders.

Fixed Costs

The usual fixed costs are equipment depreciation, interest, insurance and taxes. Depreciation is a way of recognizing the decline of value of a machine as it is working over its economic life. While this is not a cash expense in most organics processing facilities, it is a cost. Depreciation schedules vary from the simplest approach, which is a straight line decline in value, to more sophisticated techniques which recognize the changing rate of value loss over time. The formula for the annual depreciation charge using the assumption of straight line decline in value is:

D = (P’ – S)/N

where D = annual depreciation charge in dollars per year, P’ is the purchase price less consumables like tires, S = salvage value, or price the machine can be sold for at the time of its disposal and N = number of years of economic life.

Economic life is the period of time that a machine can operate at an acceptable operating cost and productivity and is greatly influenced by working conditions. For example, a loader could have a life of 10,000 to 15,000 hours depending on conditions of use, after which point the cost of maintaining the loader becomes too excessive. Expressed in years, economic life is calculated by defining the number of working days per year and the number of working hours per day.

For example, a horizontal grinder costs $350,000 and has an expected life of 8 years. Assuming a salvage value of 10 percent ($35,000) and that 5 percent of the purchase price reflects consumables ($17,500), the annual depreciation charge is:

D = ($332,500 – $35,000)/

8 years = $37,187.50/year

and if the grinder is used 4 hours/day, 5 days/week (1,040 hours/year), the hourly depreciation rate is $35.75.

Interest costs are the costs of using funds to buy equipment. For loans from investors or financial institutions, interest costs may be included in the loan documents, or can be calculated as the interest rate per year multiplied by the amount of the loan multiplied by the number of years to repay the loan (another method is to multiply the loan rate by the average annual investment). For equipment purchased with cash, the interest cost is the rate that would have been earned if that money were invested elsewhere multiplied by the equipment cost multiplied by the number of years of a typical equipment loan, usually 5 years. If equipment is leased, the monthly lease rate is used as the basis for the annual interest cost. Using the same horizontal grinder example as above, assuming a loan from a private investor at 10 percent for 5 years, the fixed-rate annual interest charge would be:

$350,000 x 10% /

5 years = $7,000/year

and the hourly interest charge would be $7,000/1,040 hours = $6.73.

Taxes are usually imposed on equipment by the local jurisdiction in which the equipment is primarily stored and used. In the author’s jurisdiction, the Machinery and Tools tax is $1.80 per $100 of value for 50 percent of the capital cost, or in the example of the horizontal grinder:

$350,000 x 50% =

$175,000 taxable capital cost

$175,000/$100 = 1,750 taxable units

1,750 taxable units x $1.80/unit/year = $3,150/year

and the hourly taxes charge would be $3,150/1,040 hours/year = $3.03.

Most private equipment owners will have one or more insurance policies against damage, fire and other destructive events. Public owners and some large owners may be self-insured. Given the wide variety of insurance coverages available, a good rule of thumb for insurance cost is 0.5 percent of the capital cost per year, or:

$350,000 x 0.5%/year = $1,750/year

and the hourly insurance charge would be $1,750/1,040 hours = $1.68.

Using the above examples, the total hourly fixed costs of owning and operating a horizontal grinder would be:

$35.75+$6.73+$3.03+$1.68

= $47.19/hour.

Operating Costs

Operating costs, unlike fixed costs, change in proportion to hours of operation or use. The actual operating costs can vary while a piece of equipment performs a single function. For example, the operating cost of a compost delivery truck is less while it is being loaded with the driver and engine idling than it would be while in transit, although tracking the data and refining the operating cost estimates to that level of detail is rarely worth the effort.

Maintenance and repair includes everything from simple maintenance to the periodic overhaul of engine, transmission, clutch, brakes and other major equipment components, for which wear primarily occurs on a basis proportional to use. Operator use or abuse of equipment, the severity of the working conditions, maintenance and repair policies, and the basic equipment design and quality all affect maintenance and repair costs. All major equipment manufacturers who supply the organics recycling industry provide spreadsheet models that describe likely hourly costs of operation. For the horizontal grinder example used above, one manufacturer estimates repair and maintenance costs at $16.03/hour; another uses $20.60/hour. Using an average of those two estimates, the hourly cost of maintenance and repair would be $18.32.

The fuel consumption rate for a piece of equipment depends on the engine size, load factor, the condition of the equipment, operator’s habit, environmental conditions, and the basic equipment design. Most horizontal grinders consume between 22 and 28 gallons per hour, so with off-highway diesel fuel costs of $2.55 per gallon, the hourly fuel cost of the horizontal grinder is about $63.75 (based on 25 gal/hr usage). Similarly, lubricants and filters maintenance costs vary due to many of the same factors that influence fuel costs. One manufacturer estimates hourly horizontal grinder grease, oil and filters costs of $4.16.

Tires are another component of operating costs. Tire life depends in part on the working surface and can vary from 750 to 4,500 hours depending on the operating conditions. One common tire size for a horizontal grinder is 385/65R22.5, which can cost from $400 to $600 each. Assuming two tires get replaced each year at $600 each, hourly tire costs could be $1.15.

Using the above examples, the total hourly operating cost for a horizontal grinder would be $18.32+$63.75+$4.16+

$1.15 = $87.38/hour.

Labor costs should be estimated with an assumption on work efficiency, as few employees actually perform a full eight hours of work per day due to interruptions, bathroom breaks and other small diversions that don’t get recorded on a timesheet. In his operations cost estimates, the author uses an efficiency estimate of 85 percent, or 6.8 actual work hours per day. If the horizontal grinder operator earns $10.00/hour ($20,800/year), and after accounting for Social Security and Medicare taxes, and Federal and State Unemployment, that cost rises to $12.20/hour. Adjusting for 85 percent work efficiency means that employee is costing the facility $14.34/hour.

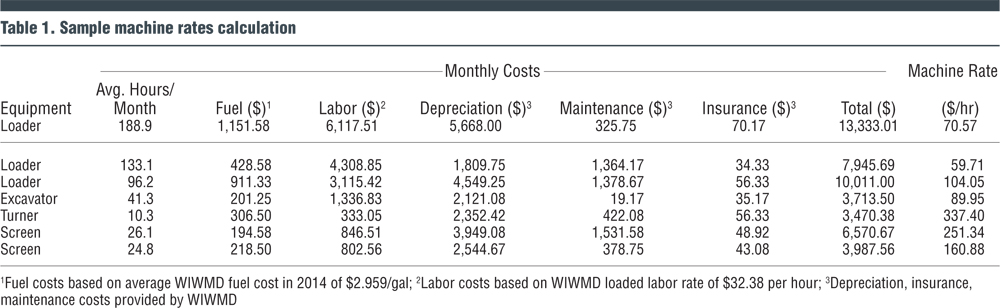

In total, the machine rate for the grinder is $47.19/hour in fixed costs, $87.38/hour in operating costs and $14.34/hour in labor costs for a total of $148.91/hour. Based on an estimate of 1,040 operating hours per year, the annual budget for that machine is $154,866. Other examples of machine rates are shown in Table 1, based on work the author did recently for the Wasatch Integrated Waste Management District in Layton, Utah, which operates a 20,000 tons/year yard trimmings composting facility.

By repeating this type of analysis for every piece of equipment involved in making products from compostable/digestible feedstocks, facility managers can develop a clear understanding of their operating costs in order to support budget requests, financial reports, and purchasing decisions.

Craig Coker is a Contributing Editor to BioCycle and a Principal in the firm Coker Composting & Consulting (www.cokercompost.com), near Roanoke, Virginia. He can be reached at craigcoker@comcast.net.