Top: Trenton Biogas processes commercial, municipal, industrial, and agricultural food waste streams in the facility’s digesters. Photo courtesy of Trenton Renewables

Paula Luu

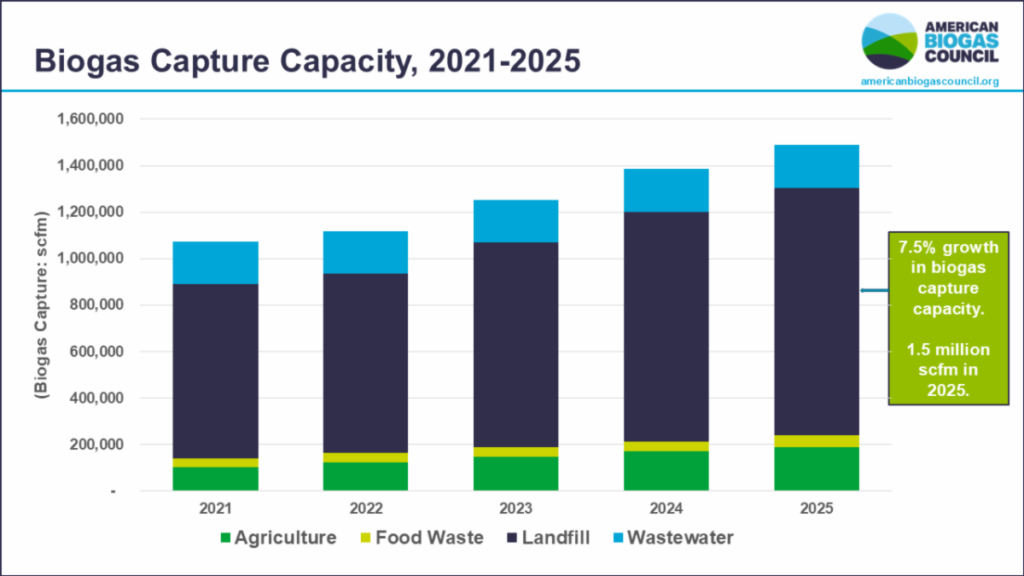

Investment in new U.S. biogas infrastructure surpassed $2 billion in 2025, reflecting continued expansion for a sector that converts organic waste into renewable energy, fuels, and soil products. New data released by the American Biogas Council (ABC) shows that 70 new biogas projects came online during the year, bringing the total number of operational biogas capture systems in the United States to roughly 2,585 facilities nationwide while increasing industrywide capture capacity by about 7.5%.

Figure 1. Growth in U.S. Biogas Capture Capacity, 2021–2025

Source: American Biogas Coalition 2026 Briefing

The $2.1 billion invested in projects completed during 2025 represents about 6% increase in capital spending over all previous capital investment. The figures illustrate steady momentum for a sector that continues to expand its role in both organics recycling and renewable energy production. While annual project counts can fluctuate with policy cycles and financing conditions, the longer term trajectory for biogas development in the United States has remained consistently upward. Patrick Serfass, Executive Director of the ABC, said the industry’s growth reflects increasing recognition that organic waste streams represent an important domestic energy resource.

Landfills Still Produce Most Captured Gas

Biogas systems operate across several sectors including wastewater treatment plants, agricultural operations, landfills, and facilities that process food waste. Nearly half of all U.S. biogas capture systems are located at wastewater treatment plants, reflecting the long history of anaerobic digestion in municipal wastewater infrastructure. Agricultural digesters and landfill gas projects represent roughly similar shares of the remaining facilities, while stand alone food waste digesters account for a smaller but growing portion of the market.

Although wastewater plants host the largest number of systems, landfill projects generate the majority of captured gas, according to ABC data. Landfill gas systems account for roughly 72% of the nation’s total biogas capture capacity.

This reflects the scale of landfill operations. Even smaller landfills can produce substantial methane volumes compared with digesters operating at farms or municipal facilities.

Figure 2. U.S. Biogas Capture Capacity by Sector (2025)

Source: American Biogas Coalition 2026 Briefing

Renewable Natural Gas Continues Rapid Expansion

One of the most important developments shaping the biogas industry is the rapid expansion of renewable natural gas production. Renewable natural gas, often referred to as RNG, is created when methane captured from organic waste streams is purified and upgraded to pipeline quality. The fuel can then be injected into natural gas pipelines or used as a low carbon transportation fuel.

The number of U.S. facilities producing RNG has grown dramatically in recent years – from 217 in 2020 to 659 by the end of 2025, representing a 3x increase over five years. Production capacity has expanded quickly as well. Total RNG output capacity roughly doubled between 2022 and 2025 as developers focused on projects serving transportation fuel markets.

This expansion has been driven largely by policies designed to reduce carbon emissions from transportation fuels. Programs such as California’s Low Carbon Fuel Standard and the federal Renewable Fuel Standard have created strong demand for fuels with lower lifecycle greenhouse gas emissions. Those incentives have helped accelerate investment in biogas systems capable of producing RNG rather than electricity.

Agriculture and Wastewater Present Major Growth Opportunities

While landfill systems remain the largest source of captured methane today, agricultural and wastewater sectors represent some of the greatest opportunities for expansion. Dairy farms dominate the agricultural digester landscape because manure from dairy operations contains significant methane potential suitable for energy production. Yet adoption rates remain relatively low.

According to the ABC data, only about 16% of U.S. dairy farms with more than 500 cows currently operate anaerobic digesters. Thousands of farms therefore remain candidates for biogas capture systems capable of producing renewable energy while improving manure management.

Wastewater treatment plants present a similar opportunity. Roughly 24% of facilities large enough to support anaerobic digestion currently capture and use biogas. Many smaller plants still flare methane produced during treatment processes instead of converting it into usable energy.

Food waste represents another major growth area. Currently, 124 stand alone digesters that process food waste streams are operating in the U.S., processing feedstocks ranging from commercial food scraps to industrial byproducts from food and beverage manufacturing. Some of these digesters are used by food and beverage manufacturers solely for their own operations.

Large Untapped Resource Remains

Despite steady growth in recent years, the United States has only begun to capture the energy potential contained in organic waste streams. Each year the country produces more than 120 million dry tons of animal manure, about 12 million dry tons of wastewater biosolids, and more than 24 million dry tons of inedible food waste that is still sent to landfills.

In addition, more than 470 landfills currently flare methane that could potentially be captured and converted into energy. According to the ABC, more than 17,000 additional biogas systems could be built nationwide if these waste streams were fully utilized.

Such expansion could generate as much as 25 gigawatts of dispatchable renewable electricity while creating approximately 900,000 construction jobs and supporting about 45,000 permanent operations positions across the country.

Serfass said the scale of that opportunity remains one of the defining characteristics of the biogas sector’s future growth. “The potential energy of the industry is massive,” he said during a briefing on the report. “There are hundreds of millions of dollars of projects that are designed and shovel ready. They are just waiting for changes in the current market conditions to move forward.”

State Level Investment Expands

Biogas investment was widely distributed across the country in 2025, with projects operating in every U.S. state. Several regions attracted particularly strong capital flows as developers pursued projects tied to local feedstocks and energy markets.

Seven states each attracted more than $100 million in biogas project investment during the year. Texas, California, Illinois, Idaho, Washington, Wisconsin, and Florida led the nation in capital spending on new systems. These states reflect a mix of policy environments, agricultural resources, and organic waste streams that support project development.

The geographic spread of investment underscores the national scale of the industry. From dairy digesters in agricultural regions to landfill gas recovery systems serving metropolitan areas, biogas infrastructure is expanding across a wide range of communities.

Emerging Energy Markets Could Shape the Next Phase

Looking ahead, industry leaders say the next phase of development may be influenced as much by energy markets as by waste management trends. Rapidly growing electricity demand associated with data centers, artificial intelligence infrastructure, and domestic manufacturing are increasing interest in reliable clean power sources that can operate continuously. Biogas-fueled power generation can provide around the clock electricity while reducing methane emissions from organic waste streams.

“Biogas fits squarely into the energy dominance conversation,” said Serfass. “We are using domestic feedstocks to produce domestic energy and fertilizer products, and much of that infrastructure is located in rural communities where the economic benefits stay local.”

Digestate produced during anaerobic digestion is also receiving greater attention as a domestic source of nutrients and soil amendments for agriculture. As these markets develop and policy frameworks evolve, developers expect investment in biogas systems to continue expanding.